What Could the Potential Loss of Insurance Mean for a California Home Transaction?

It's not news that premiums have increased and that areas of wild fires have seen a pullback from insurance companies. The refusal by insurance companies is not just in climate zones, many types of properties are now affected, including areas that are low risk of fire and flood.

If you're a buyer or seller and currently in a transaction, be aware that the buyer contingency in a standard California Association of Realtors contract allows for investigation of the property, including insurance issues that may prevent coverage. This is very important that the buyer understand their contracts, and follow up completely on insurance coverage. Under standard timelines, the buyer contingencies are removed assuming the buyer is satisfied with various areas of investigation. However, since lenders offering a mortgage want to see proof of insurance coverage prior to close of escrow, buyers are strongly advised to obtain an insurance binder or evidence of commitment to insurance coverage as soon as possible in the escrow period (the 1st day it opens), and not remove their buyer contingency until they know they will have insurance policy on that property. Otherwise, they may risk losing their buyer deposit under the terms of their contact with the seller.

Homeowner associations are seeing increases in their master policy premiums, changes in coverage limits, or a refusal to renew policies. If an HOA master policy isn't renewed, then the mortgages of the condominiums owners are also at risk, since lenders want proof of that policy coverage for the common areas. Or, in the case of some associations, the increase in premium may be so huge it causes a special assessment: one HOA reported in the San Diego Union Tribune ended up with an $8,000 per unit cost for master policy insurance coverage.

If you're a homeowner with current coverage, do not let it lapse, because it may not be renewed. The California Fair Plan may be an option for some residents and businesses; it protects the home for fire risk and will satisfy a mortgage company's insurance requirement, but it does not cover theft, flood, earthquake, hail, vandalism or personal liability (only special earthquake policy provides coverage for that).

Insurance brokers are reporting challenging coverage searches for their clients, and are not always successful. The one area of insurance so far not reporting a problem is renters insurance, which does not cover fire risk.

If you are not currently represented by a Realtor in a transaction and are interested in finding out what the buyer contingencies are in a purchase transaction, please contact me via phone, text or email.

Julia Huntsman, REALTOR, Broker | http://www.juliahuntsman.com | 562-896-2609 | California Lic. #01188996

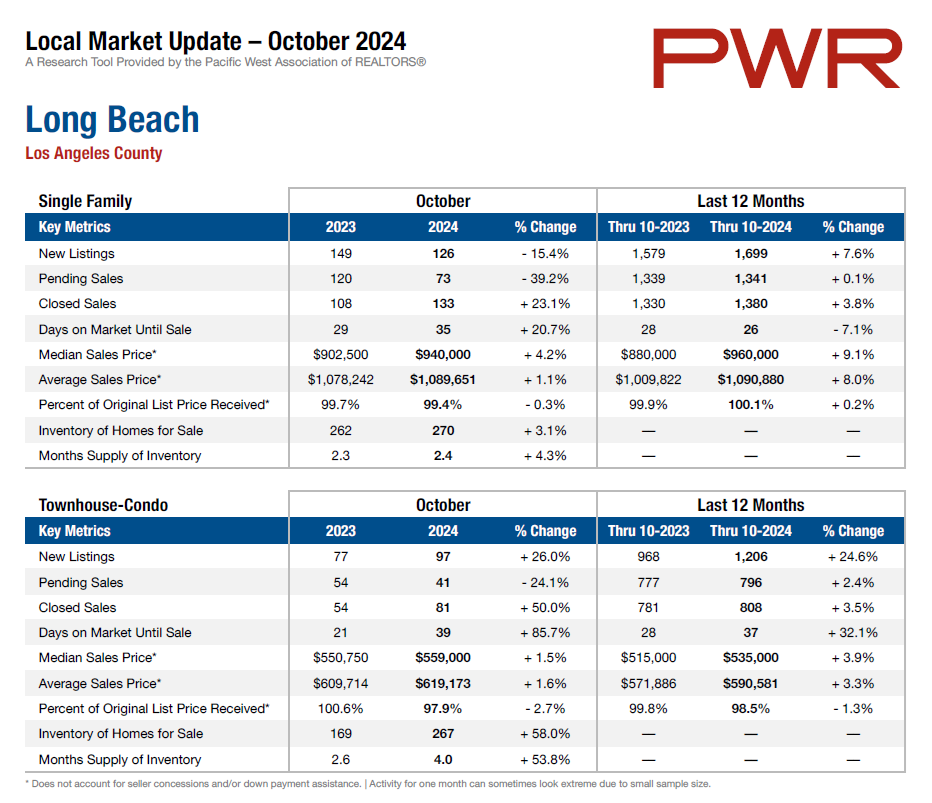

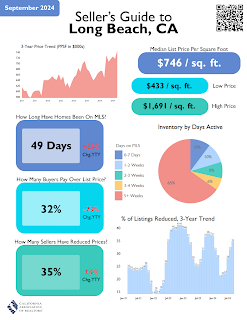

Your Market Info